Market Overview

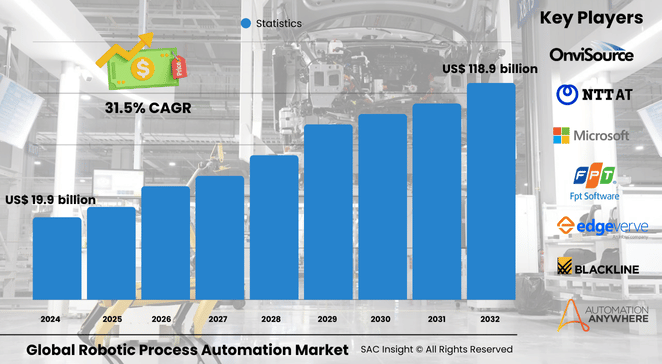

The global robotic process automation (RPA) market size stood at US$ 19.985 billion in 2024 and is on track to surge to roughly US$ 118.99 billion by 2032, registering a fast-paced 31.05% CAGR over the 2025-2032 forecast window. Heightened pressure to cut costs, shrink error rates, and redeploy talent from mundane tasks to higher-value workstreams is accelerating adoption across banking, healthcare, logistics, and public services. First-hand industry insights highlight that cloud-native, AI-enhanced bots now handle multi-step workflows once considered too complex for rule-based automation, setting the stage for double-digit market growth in every major region.

In the United States robotic process automation (RPA) market alone, federal initiatives that freed 1.5 million staff hours underscore the tangible gains driving national market share expansion.

Summary of Market Trends & Drivers

• Service-centric delivery models (RPA-as-a-Service, managed bots) are overtaking perpetual licenses as buyers seek quick starts and predictable costs.

• Integrating AI, computer vision, and natural-language capabilities into bots is shifting demand from simple rule execution toward "intelligent" automation that can read unstructured data, make decisions, and self-heal.

• A growing focus on governance, security, and sustainability is prompting enterprises to pair RPA with robust compliance tooling and carbon-aware cloud platforms.

Key Market Players

Global leadership rests with a mix of pure-play RPA specialists and enterprise software giants. UiPath, Automation Anywhere, and Blue Prism continue to command the largest installed bases, thanks to expansive bot libraries and strong partner ecosystems. Meanwhile, Microsoft, SAP, and Pegasystems leverage deep application footprints to bundle automation into wider digital transformation deals. Emerging contenders such as NICE, WorkFusion, and Uniphore are sharpening their edge in vertical AI models, conversational automation, and document understanding, pushing incumbents toward faster product refreshes and targeted M&A to defend market share.

Key Takeaways

• Market value (2024): USd$ 19.985 billion

• Projected value (2032): USD$ 118.99 billion at a 31.05% CAGR

• Services dominate, capturing about 64% of 2024 revenue, powered by RPA-as-a-Service demand

• Cloud deployment already exceeds 53% market share and is widening its lead as SaaS pricing lowers entry barriers

• BFSI remains the single largest end-use vertical, while healthcare shows the strongest incremental growth as digital health investments scale

• North America accounted for just over 39% of global revenue in 2024, buoyed by aggressive automation targets in finance and federal agencies

Market Dynamics

Drivers

• Urgent need to improve operational efficiency and time-to-value in a high-inflation, talent-scarce environment

• Rapid advances in AI and machine-learning toolsets that extend bot capabilities to judgement-intensive tasks

• Proliferation of cloud marketplaces and pre-built connectors that shorten deployment cycles

Restraints

• Upfront change-management and infrastructure investments can deter smaller firms despite falling bot prices

• Fragmented legacy systems may require extensive integration work, delaying returns

• Ongoing skills gaps in bot design and governance raise risk of sprawl and security misconfigurations

Opportunities

• Verticalized solutions for healthcare claims, pharma pharmacovigilance, and telecom order management remain under-penetrated

• Low-code development platforms can open RPA to business users, expanding addressable market size

• Carbon-tracking features in bots give providers an edge with ESG-focused buyers

Challenges

• Intensifying price competition among vendors threatens margins and complicates long-term support economics

• Regulatory scrutiny of algorithmic decision-making could slow approvals in highly regulated industries

• Measuring and sustaining true enterprise-wide productivity gains beyond pilot projects remains difficult

Regional Analysis

North America robotic process automation market leads the global landscape on the back of large enterprise budgets, mature cloud adoption, and robust compliance needs. Europe follows, catalyzed by cost-out mandates and stringent data-protection rules that favor on-premises and sovereign-cloud deployments. Asia-Pacific is the fastest-growing territory as banks, insurers, and manufacturers in China, India, and Japan pivot from legacy macro-scripts to modern RPA-AI hybrids.

• North America – First-mover advantage, strong federal and BFSI uptake

• Europe – Rising intelligent automation, cost savings of 30-50% cited by SMEs

• Asia-Pacific – Highest regional CAGR, fueled by industrial digitization and skilled IT labor pools

• Latin America – Growing interest in SaaS bots to bypass capex constraints

• Middle East & Africa – Early deployments in government and energy, with skills training on the rise

Segmentation Analysis

By Component

• Services – Largest revenue contributor

Services encompass assessment, deployment, and ongoing support, giving enterprises turnkey capabilities and faster ROI without heavy internal resourcing.

• Software – Fast-growing on the back of partnerships

Platform vendors are opening app marketplaces and freemium tiers, expanding reach among developers and business analysts alike.

By Deployment

• Cloud – Majority share and expanding

Subscription pricing, scalability, and remote management make cloud the default choice for new projects, especially among distributed teams and midsize firms.

• On-premise – Resilient niche

Data-sovereignty rules, bespoke security policies, and tight integration with mainframes keep on-premise installations relevant in banking and government.

By Enterprise Size

• Large Enterprises – Early adopters, deep automation roadmaps

Fortune 500 firms leverage bots at scale to handle millions of transactions, driving demand for advanced analytics and governance modules.

• Small & Medium Enterprises – Fastest relative growth

Simplified SaaS offerings and pay-per-bot models let SMEs tap RPA for tasks like invoice capture and payroll, unlocking quick wins without large IT teams.

By Operations

• Rule-Based – Widest installed base

Perfect for high-volume, deterministic processes such as data entry and report generation, rule-based bots integrate smoothly with legacy systems.

• Knowledge-Based – Rapidly emerging

Infused with AI and natural-language understanding, these bots tackle dynamic, exception-heavy work such as claims adjudication and customer e-mail triage.

By End Use

• BFSI – Core demand engine

Banks and insurers automate KYC checks, loan processing, and fraud monitoring to cut turnaround times and meet compliance deadlines.

• Pharma & Healthcare – Strong forecast CAGR

Clinical documentation, claims pre-authorization, and lab scheduling are prime use cases as providers chase accuracy and patient-centric care.

• Retail & Consumer Goods – Growing omni-channel pressure

Bots handle order reconciliation, inventory updates, and after-sales queries, freeing staff for personalized engagements.

• IT & Telecom, Manufacturing, Logistics, Energy & Utilities, and Others – Diverse adoption

From service-desk ticket triage to production line analytics, RPA supports continuous-improvement agendas across industries.

Industry Developments & Instances

• December 2024 – UiPath joined forces with a UAE government office to roll out agentic automation and upskill 100 public-sector employees.

• November 2024 – Automation Anywhere and PwC India launched generative AI automation solutions for banking, retail, and healthcare clients.

• October 2024 – Omega Healthcare reported 60 million transactions processed via UiPath bots, demonstrating large-scale ROI in clinical documentation.

• May 2024 – PathAI introduced an RPA-ready image-management platform for European pathology labs, signaling the intersection of AI and automation.

• November 2023 – OnviSource partnered with TForge to embed AI-powered analytics into South-African contact centers.

Facts & Figures

• Services captured 64% of global revenue in 2024.

• Cloud deployments crossed the 53% threshold the same year and continued to climb.

• Average cost savings cited by European SMEs reached 50%, versus 30% for large enterprises.

• Federal U.S. RPA programs freed 1.5 million staff hours between 2020 and 2023.

• Administration and reporting applications account for the bulk of bot licenses, while AI-enabled data-analysis use cases show the fastest uptake.

• North America held over 39% market share in 2024, with Asia-Pacific registering strong regional CAGR.

Analyst Review & Recommendations

SAC Insight's deep market analysis confirms that RPA is shifting from tactical cost-cutting to strategic digital enablement. Vendors that combine low-code design, AI orchestration, and airtight governance will capture outsized market growth as buyers consolidate around full-stack platforms. Enterprises should invest early in center-of-excellence frameworks and bot-lifecycle management to avoid fragmentation and secure sustainable returns as automation scales across functions.