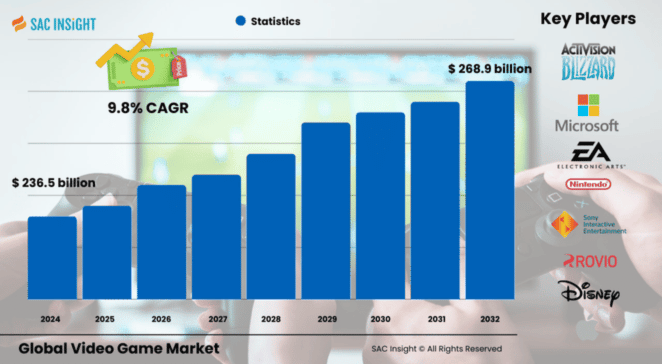

Market Overview

The global video game market size was approximately US$ 236.5 billion in 2024 and is set to grow to around US$ 268.9 billion by 2025. Forward-looking market analysis suggests the sector will increase to nearly US$ 541 billion by 2032, expanding at an average CAGR of 9.85% over the 2025-2032 forecast window. This sustained market growth is driven by increasing smartphone penetration, mainstream acceptance of esports, and industry insights indicating that cloud and 5G connectivity are transforming how, where, and with whom people play.

In the United States video game segment alone, the market size is projected to reach approximately US$ 67.6 billion by 2032, underscoring the region's high spending power and appetite for premium content.

Summary of Market Trends & Drivers

• Competitive multiplayer and esports tournaments are transitioning from niche to mass-audience entertainment, driving longer playtimes and in-game spending.

• The rapid adoption of 5G and cloud gaming removes hardware barriers, allowing casual players to access high-fidelity titles on mid-range devices.

• Immersive technologies such as augmented and virtual reality are elevating engagement levels, while live-service models keep franchises relevant for years.

Key Market Players

Leading publishers and platform owners continue to shape market share through blockbuster IP, ecosystem lock-in, and aggressive M&A. Console heavyweights Sony Interactive Entertainment, Microsoft, and Nintendo compete head-to-head on exclusive titles and subscription services, while Tencent, Activision Blizzard, and Electronic Arts leverage massive multiplayer communities to maintain stickiness.

On the hardware and distribution side, Apple, Google, and NVIDIA exploit mobile operating systems and cloud infrastructure to keep users within their service stacks. A cohort of fast-moving studios such as Epic Games, Ubisoft, Bandai Namco, Lucid Games, and Rovio is pushing cross-platform releases and free-to-play monetisation to capture incremental audiences.

Key Takeaways

• Current global market value (2024): USD$ 236.5 billion

• Projected global value (2032): USD$ 541 billion at a 9.85% CAGR

• Asia-Pacific commands the largest regional market share at about 50% and is the fastest-growing territory

• Mobile gaming already accounts for roughly 40% of global revenue, outpacing consoles and PCs

• Online titles dominate with a 44% share, propelled by live-service models and social play

• The U.S. remains the single most lucrative national market, forecast to eclipse US$ 67 billion by 2032

Market Dynamics

Drivers

• Ubiquitous smartphones and inexpensive data plans widen the addressable player base.

• Esports viewership and sponsorship money elevate gaming into mainstream media.

• Cloud platforms lower entry costs, letting premium games reach mid-tier devices.

Restraints

• Health concerns, government play-time restrictions, and data-privacy rules curb engagement in some countries.

• Cyber-security risks and cheating scandals erode trust and can dampen monetisation.

Opportunities

• Subscription bundles and cross-media IP extensions (films, series, toys) diversify revenue.

• AR/VR hardware price drops open doors for new immersive genres and enterprise training spin-offs.

Challenges

• Intensifying competition for screen time with short-form video and social media.

• Rising development budgets and talent shortages increase financial risk for AAA titles.

Regional Analysis

Asia-Pacific dominates thanks to population scale, mobile-first habits, and strong local publishers, while North America benefits from high ARPU and early adoption of cutting-edge tech. Europe holds steady with diversified platforms and robust regulation that fosters consumer confidence.

• Asia-Pacific – Half the global revenue, double-digit CAGR driven by China, Japan, South Korea, and rapidly growing India.

• North America – Roughly one-quarter share, buoyed by subscription services and premium console launches.

• Europe – Solid mid-teens share; GDPR compliance and cultural diversity shape content strategies.

• Latin America – Rising disposable incomes and esports arenas fuel above-average growth.

• Middle East & Africa – Smaller base but expanding mobile networks create long-term upside.

Segmentation Analysis

By Device

• Mobile – Cornerstone of user expansion Mobile titles combine convenience and low cost, giving publishers the largest potential audience and the most granular monetisation levers, from cosmetics to battle passes.

• Console – Premium, immersive experience Hardware upgrades to 4K/120 Hz, SSDs, and haptic controllers keep consoles relevant for households seeking cinematic storytelling and split-screen social play.

• Computer/PC – Competitive and mod-friendly hub High-end GPUs, moddable ecosystems, and esports pedigree position PCs as the platform of choice for serious competitors and content creators.

By Platform Type

• Online – Growth engine of the industry

Live-services, microtransactions, and community events sustain engagement and recurring revenue, making online the dominant platform segment.

• Offline – Narrative depth and ownership appeal Single-player epics and collectible physical editions continue to attract enthusiasts who value immersive storytelling without bandwidth dependencies.

By Age Group

• Generation Z – Core driver of digital consumption Gen Z grew up with smartphones and streams gameplay as social currency, amplifying viral hits and shaping market trends.

• Generation Y (Millennials) – Spending power meets nostalgia Millennials balance premium console purchases with mobile convenience, often revisiting classic IP reboots.

• Generation X – Niche yet loyal audience Gen X gravitates toward consoles and PCs, supporting remastered franchises and high-fidelity simulators.

Industry Developments & Instances

• January 2022 – AT&T teamed with a major GPU provider to bundle 5G cloud gaming access across more than 100 high-end titles.

• February 2022 – Tencent broadened its global footprint by acquiring significant stakes in European and North American studios.

• June 2023 – A leading publisher launched Super Mega Baseball 4, showcasing next-gen presentation upgrades that boost spectator appeal.

• September 2022 – India’s first dedicated university esports arena opened with a US$ 98 million investment, signalling academia’s embrace of gaming careers.

• October 2022 – A AAA shooter sequel debuted free-to-play with aggressive monetisation, underlining the shift toward live-service economics.

• July 2022 – Major smartphone brands rolled out gaming-centric models featuring 165 Hz displays and active cooling to court mobile esports athletes.

Facts & Figures

• Approximately 3.22 billion people played video games in 2023, and that base is expected to exceed 3.4 billion by 2025.

• Asia-Pacific captures around 50.4% of global revenue, reflecting both spending power and player count.

• Mobile devices generated a 40% market share in 2022 and continue to outpace console revenue growth.

• The average mobile gamer is 36.3 years old, and 86% of Gen Z plays games on smartphones.

• Esports events routinely surpass 5 million concurrent viewers, rivaling traditional sports broadcasts.

Analyst Review & Recommendations

SAC Insight's deep market evaluation shows that cross-platform ecosystems and live-service design will remain the heartbeat of video-game monetisation. Publishers should double down on mobile-first strategies for emerging markets while pairing premium console and PC releases with robust social and competitive features. Hardware vendors that integrate cloud streaming and affordable AR/VR accessories can unlock fresh demand curves. Long-term success hinges on balancing player wellness with engagement, tightening cyber-security, and localising content to navigate an increasingly complex regulatory map.