Market Overview

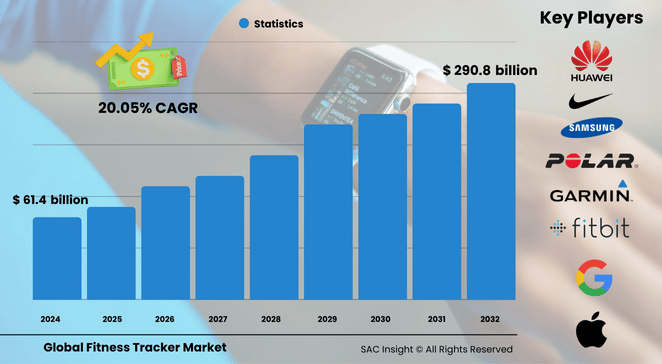

The fitness tracker market size was valued at US$ 61.47 billion in 2024 and is forecast to reach US$ 290.85 billion by 2032, clocking a vigorous 20.05% CAGR from 2025-2032. First-hand industry insights point to three structural tailwinds: consumer focus on preventive health, corporate wellness investments, and rapid sensor innovation that folds medical-grade metrics into everyday wearables. SAC Insight's deep market evaluation shows North America holding 41.7% market share with revenues of US$ 29.28 billion in 2024; at the same growth pace, the region is set to top roughly US$ 135.30 billion by 2032.

Summary of Market Trends & Drivers

• Continuous glucose, blood-pressure, and stress monitoring are pushing wearables beyond step counting, creating stickier engagement and higher upgrade cycles.

• Seamless pairing with mobile ecosystems and AI-powered coaching services is redefining the user experience, driving market growth across both premium and value tiers.

• Employer-sponsored fitness programs and insurer incentives are accelerating adoption, particularly in the U.S. and Europe.

Key Market Players

Global competition is led by consumer-tech heavyweights and specialist brands alike. Apple commands the premium smartwatch arena with deep health integrations, while Google’s Fitbit line retains a loyal fitness-first base. Garmin continues to dominate performance-centric niches, and Samsung, Huawei, and Xiaomi leverage multi-device ecosystems and aggressive pricing to scale rapidly. Fossil and several lifestyle labels enrich the mid-price segment through fashion-tech collaborations, sustaining vibrant product refresh cycles and keeping barriers to entry high.

Key Takeaways

• Market value (2024): USD$ 61.47 billion

• Projected value (2032): USD$ 290.85 billion at a 20.05% CAGR

• Smartwatches captured 48.5% revenue share in 2024, remaining the category growth engine

• Running tracking holds the largest single-application share at 31.4%

• Online sales account for 65% of unit volumes, reflecting widening e-commerce reach

• North America leads today; Asia-Pacific is the fastest-growing region through 2032

Market Dynamics

Drivers

• Rising prevalence of chronic conditions—obesity, diabetes, hypertension—spurs demand for continuous vital-sign monitoring.

• Broader smartphone penetration and affordable sensors lower entry costs, widening the addressable user base.

• Corporate and insurer wellness incentives boost device uptake among working-age adults.

Restraints

• Data-privacy concerns and unclear regulatory boundaries between consumer wearables and medical devices temper adoption.

• Short battery life and limited cross-platform compatibility can erode long-term user engagement.

Opportunities

• Integration of non-invasive glucose monitoring and blood-pressure measurement opens high-value healthcare partnerships.

• Emerging-market consumers seek sub-USD$ 100 smart bands, inviting local manufacturing and localized app ecosystems.

Challenges

• Chipset shortages and supply-chain disruptions raise production costs and risk stock-outs.

• Fierce price competition compresses margins, pressuring smaller brands to differentiate on software and services.

Regional Analysis

North America dominates on the back of high disposable income, tech-savvy consumers, and robust corporate wellness budgets. Europe follows, propelled by proactive public-health initiatives and growing obesity rates. Asia-Pacific is the hot-growth zone, buoyed by rising middle-class incomes and aggressive local brand launches.

• North America – largest revenue contributor; heavy corporate wellness adoption

• Europe – substantial uptake driven by chronic-disease burden and sports culture

• Asia-Pacific – fastest CAGR; smartphone ubiquity and affordable trackers fuel expansion

• Latin America – steady gains via government fitness campaigns and e-commerce growth

• Middle East & Africa – early but accelerating adoption as health awareness spreads

Segmentation Analysis

By Device Type

• Smart Watches – Sensor-rich, nearly half of market value. Smart watches marry health tracking with robust app ecosystems, making them the default choice for tech-conscious users and driving recurring service revenues for vendors.

• Fitness Bands – Budget-friendly, long battery life. Bands focus on core metrics—steps, heart rate, sleep—at entry-level prices, attracting first-time buyers and corporate wellness bulk purchases.

• Smart Glasses – Niche augmented-fitness plays. Heads-up displays deliver real-time performance stats for cyclists and runners, though high prices keep volumes modest.

• Smart Clothing – Emerging segment for biomechanical analytics. Embedded sensors in shirts and shoes offer granular gait, posture, and muscle-load insights, appealing to professional athletes and physiotherapists.

• Others – Clip-ons and hybrid analog trackers. Specialized form factors serve seniors, kids, and clinical-trial participants where wrist wear is impractical.

By Application

• Running Tracking – Core demand engine with 31.4% share. GPS accuracy and personalized coaching plans make running the flagship use case across genders and ages.

• Heart Rate Tracking – Default health metric. Continuous heart-rate sampling underpins calorie burn, stress analysis, and arrhythmia alerts, driving cross-segment utility.

• Sleep Measurement – Rising focus on recovery. Advanced algorithms translate motion and heart-rate variability into actionable sleep-stage guidance.

• Glucose Measurement – High-potential breakthrough. Non-invasive sensors in pilot stages aim to bring diabetes monitoring to the mass market.

• Sports & Cycling Tracking – Performance-level insights. Multisport modes, VO2 max estimates, and power-meter integrations cater to triathletes and cyclists seeking edge data.

By Wearing Style

• Hand Wear – Dominant at 72.3% share. Wrist-based devices offer intuitive displays and easy interaction, reinforcing their market leadership.

• Leg Wear – Fastest-growing for smart shoes. Shoe-embedded sensors deliver stride analytics and fall detection, resonating with runners and elder-care providers.

• Head Wear – Specialized in AR and biomechanics. Smart headbands and helmets capture brain-wave or positional data, targeting niche sports and wellness segments.

• Others – Clip-ons and patches. Alternative placements meet workplace safety or medical-trial requirements.

By Distribution Channel

• Online – 65% share, highest growth. Direct-to-consumer websites and e-commerce giants provide price transparency, fast shipping, and easy comparisons.

• Retail – In-store trials and expert advice. Physical outlets remain vital for experiential demos, bundling offers, and instant fulfillment, especially during holiday seasons.

• Others – Corporate and healthcare procurement. Bulk orders for wellness programs and hospital initiatives create steady volume streams.

Industry Developments & Instances

• September 2024 – Masimo and Qualcomm unveiled a next-gen smartwatch platform for Wear OS, promising clinical-grade pulse oximetry.

• July 2024 – KORE and mCare Digital launched the mCareWatch 241 for remote patient monitoring with fall detection and geo-fencing.

• February 2024 – Samsung released Galaxy Fit 3 with 100+ workout modes and SpO2-based sleep scoring.

• October 2023 – Xiaomi rolled out Smart Band 9 Pro featuring integrated GPS and 150 sports modes.

• September 2023 – Google introduced Fitbit Charge 6, touting improved heart-rate precision powered by device-side machine learning.

• January 2023 – Garmin secured FDA clearance for its ECG app on Venu 2 Plus, strengthening its clinical credentials.

Facts & Figures

• Roughly 4.88 billion people worldwide own smartphones, providing a vast ready-pairing base for wearables.

• Smartwatches’ average battery life improved by 25% over the past two product cycles, according to vendor benchmarks.

• 92% of smartwatch users say their device helped achieve at least one fitness goal.

• Workplace wellness programs offering trackers report up to 30% reduction in sick days over two years.

• Continuous glucose monitoring wearables are projected to reach 10% penetration of diabetic adults by 2030.

Analyst Review & Recommendations

Fitness trackers are evolving from simple pedometers into multi-sensor health hubs that sit at the intersection of consumer tech and digital medicine. Players that combine accurate biometrics with AI-driven coaching and airtight privacy safeguards will outpace the pack. Short term, bolstering battery life and cross-platform compatibility should stay top priorities. Long term, integration with insurer and employer ecosystems will create durable revenue streams and deepen user engagement, anchoring the market’s move toward holistic, data-centric preventive care.