Market Overview

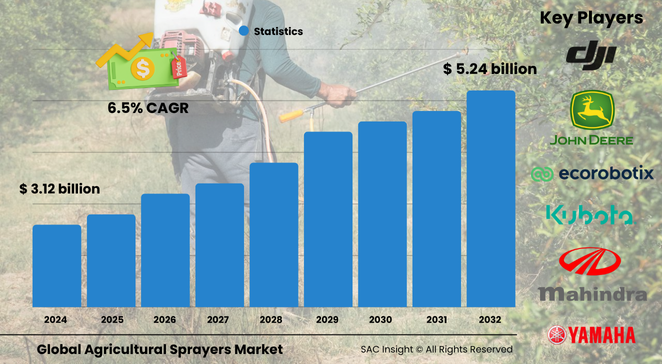

The global agricultural sprayers market size sits at roughly US$ 3.125 billion in 2024 and is projected to climb to about US$ 5.24 billion by 2032, achieving an average 6.535% CAGR. SAC Insight's industry insights highlight three powerful growth levers: the drive for higher farm productivity, rapid uptake of precision farming technologies, and rising demand for eco-efficient spraying solutions.

SAC Insight's deep market evaluation shows the United States market could approach nearly US$ 1.1 billion by 2032 as large-scale row-crop operations automate chemical application to offset labor shortages.

Summary of Market Trends & Drivers

Persistent farm-labor gaps, government subsidies for mechanization, and steady advances in drone and battery technologies are pushing market growth. At the same time, stricter residue and drift regulations are steering product innovation toward variable-rate, low-volume, and electrostatic systems that cut chemical use and boost sustainability.

Key Market Players

Leading vendors include global machinery majors known for broad dealer networks and robust R&D pipelines. Brands such as Deere, CNH Industrial, Kubota, Mahindra & Mahindra, and AGCO supply high-capacity self-propelled rigs and data-enabled front-boom models. Specialist manufacturers—EXEL Industries, Bucher, STIHL, DJI, and Yamaha—are expanding with high-precision drones, orchard sprayers, and backpack units tailored for smallholders and specialty crops. Competitive dynamics revolve around smart-spray software, autonomous navigation, and localized production to keep prices attractive for emerging-market farmers.

Key Takeaways

• Current global market size (2024): roughly USD$ 3.125 billion

• Projected global market size (2032): about USD$ 5.24 billion at a 6.535 percent CAGR

• Asia Pacific commands the largest market share, led by India, China, and Australia

• Self-propelled sprayers hold the highest revenue owing to speed, stability, and integrated telematics

• Electric & battery-driven units are the fastest-growing power-source category as costs fall

• Market trends center on precision nozzles, drone swarms, and connected fleet management

Market Dynamics

Drivers

• Growing farm sizes and pressure to maximize yield per hectare

• Widening government incentive programs for mechanization and precision spraying

• Rapid technology transfer of GPS, AI vision, and IoT into mainstream farm equipment

Restraints

• High upfront cost of advanced machines limits adoption among smallholders

• Patchy rural charging infrastructure slows uptake of battery-powered models

• Volatile agrochemical prices can reduce farmer spending on new equipment

Opportunities

• Integration of sprayers with farm-management software enables real-time agronomy decisions

• Solar-assisted charging and fuel-flex engines open doors in remote regions

• Subscription-based equipment leasing models lower barriers for cash-constrained growers

Challenges

• Spray-drift regulations demand continuous nozzle calibration and user training

• Fragmented aftermarket service in developing countries weakens brand loyalty

• Component shortages—particularly semiconductors and specialty plastics—stretch lead times

Regional Analysis

Asia Pacific dominates today’s market thanks to a vast arable base, supportive subsidy schemes, and fast adoption of drone spraying in rice and orchard crops. North America follows, driven by large grain operations and stringent drift control, while Europe emphasizes environmental compliance and worker safety. Latin America and the Middle East & Africa present high upside as farm consolidation and credit programs accelerate mechanization.

• Asia Pacific – Largest revenue base; drone fleets and front-boom rigs gain traction

• North America – High self-propelled penetration and rapid battery adoption

• Europe – Tight chemical rules spur smart-spray retrofits and recycling systems

• Latin America – Sugarcane and soybean sectors drive demand for high-volume fuel sprayers

• Middle East & Africa – Emerging precision-farming hubs adopt solar-powered backpack units

Segmentation Analysis

By Type

• Self-propelled – Premium performance, highest market share.

Stability at high speed and integrated GPS guidance make these rigs indispensable for large farms aiming to finish spraying windows in narrow weather gaps.

• Tractor-mounted – Versatile mid-range option.

Mounting kits convert existing tractors into cost-effective spray platforms, ideal for mixed-crop holdings seeking flexible equipment use.

• Trailed – High-capacity value choice.

Large tanks and wide booms allow broad-acre operators to cover hectares quickly without investing in a dedicated chassis.

• Handheld – Niche but vital for spot treatments.

Backpack and knapsack designs give smallholders affordable access to crop protection, especially in hilly or fragmented plots.

• Aerial – Fastest-rising share.

Fixed-wing and multirotor drones deliver ultra-low-volume application with centimetre-level accuracy, cutting water use and operator exposure.

By Power Source

• Fuel-based – Workhorse for high-volume jobs.

Internal-combustion engines provide long run-time and the muscle to handle dense formulations, remaining dominant in broad-acre cereal belts.

• Electric & Battery-driven – Rapidly expanding.

Lithium-ion packs and brushless motors reduce noise and emissions, aligning with sustainability goals and indoor farming needs.

• Solar – Emerging eco-variant.

Panels trickle-charge batteries during idle periods, extending run-time for greenhouse and remote-orchard operations without grid access.

• Manual – Low-cost legacy.

Hand-pump sprayers persist in micro-plots and urban gardens where capital budgets are tight.

By Nozzle Type

• Hydraulic – Versatile and widely used.

They handle a broad flow-rate range, allowing easy swap-outs for different crops and chemistries.

Uniform droplet sizes make hydraulic nozzles suitable for cereals, oilseeds, and broadleaf vegetables.

• Gaseous – Drift-reducing specialist.

Air-induction designs create large, air-filled droplets that resist off-target movement in windy conditions.

• Centrifugal – Precision micro-dose tool.

Spinning-disc heads generate fine, consistent droplets for ultra-low-volume work on high-value horticultural crops.

• Thermal – Targeted weed control.

Heat-based atomization supports herbicide formulations that require minimal carrier water, aiding desert farming where water is scarce.

By Capacity

• High volume – Preferred for broad-acre grain.

Tanks exceeding 1,500 litres cut refill downtime, critical during narrow herbicide application windows.

• Low volume – Balanced flexibility.

Mid-sized tanks suit diversified farms juggling cereals, pulses, and vegetables.

• Ultra-low volume – Water-saving niche.

Droplet atomizers enable coverage with as little as 5 litres per hectare, prized in drought-prone regions.

By Usage

• Field sprayers – Core demand engine.

Large boom widths deliver uniform coverage on wheat, corn, and soybean fields, driving the bulk of global sales.

Field units now integrate on-board sensors to vary dose by canopy density, maximizing return on chemical spend.

• Orchards sprayers – Growing specialty segment.

Air-blast and tower configurations push droplets into dense canopies, helping fruit growers combat fungal outbreaks.

• Garden sprayers – Small but steady.

Hobby farms and landscape services favour lightweight cordless models for spot treatment and fertilizing ornamentals.

Industry Developments & Instances

• November 2022 – DJI unveiled the T50 drone with dual phased-array radar and 40 kilogram spray payload.

• October 2022 – Yamaha introduced the FAZER R AP helicopter featuring automatic flight paths for large-field spraying.

• August 2022 – Case IH launched the autonomous Trident 5550 spreader, embedding driverless technology in high-clearance chassis.

• June 2022 – Guardian front-boom series upgraded with precision controls and automatic rinse cycles.

• March 2022 – A full Patriot sprayer redesign added advanced connectivity and cab comfort upgrades.

• January 2022 – Eavision rolled out the EA-30X terrain-aware drone for hill and mountain farms.

• April 2023 – Bosch BASF Smart Farming partnered with a major OEM to commercialize AI weed-recognition sprayers from 2024.

• August 2023 – A leading Indian manufacturer opened a new plant aimed at affordable battery sprayers for smallholders.

Facts & Figures

• Asia Pacific held nearly 37 percent market share in 2022.

• Fuel-powered rigs still represent over 55 percent of global unit revenue.

• Battery prices have declined by about 60 percent since 2018, catalyzing cordless sales.

• Self-propelled sprayers can cover more than 100 hectares per hour with 36-metre booms.

• Drone spraying can cut chemical use by up to 30 percent versus conventional ground rigs.

Analyst Review & Recommendations

Our market analysis indicates a decisive pivot toward connected, resource-efficient spraying platforms. Vendors that combine modular hardware with AI-enabled drift control and flexible financing will capture outsized market share. In the near term, prioritizing mid-range electric models for emerging markets and retrofit kits for hydraulic nozzle upgrades offers quick wins. Long term, strategic investment in autonomous aerial fleets and solar-hybrid powertrains will position manufacturers for sustainable, high-margin market growth.